Braskem 1Q26: Event Risk Drives the Trade

Improved spreads and policy support provide optionality, but recovery outcomes remain tied to creditor talks and liquidity preservation

We maintain our Neutral recommendation on Braskem. 1Q26 results improved sequentially at the EBITDA level, but not enough to change the credit debate. Braskem remains a capital structure and liquidity story rather than a clean cyclical recovery story, with very high leverage, negative FFO, weak cash generation, limited working capital flexibility, and the drawn US$1.0 billion standby facility due in December 2026 still central to the refinancing discussion. We think REIQ support, the recent improvement in petrochemical spreads, and the ongoing governance reset provide important optionality, but they do not yet solve the balance sheet problem.

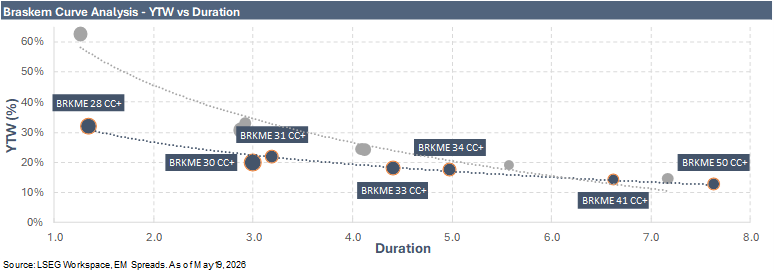

The main change since our 4Q25 downgrade is valuation. Braskem’s senior unsecured bonds have rallied materially from distressed levels, with the BRKME 4.500% 2028s now at $66.9, up from $46.9 at the time of our 4Q25 report, the BRKME 4.500% 2030s at $60.9 versus $46.4, the BRKME 8.500% 2031s at $62.1 versus $44.9, and the BRKME 5.875% 2050s at $48.3 versus $38.5. The move reflects lower perceived immediate default risk, policy support, better short-term spread expectations, and progress on the ownership and governance framework. However, the underlying credit risks remain largely unresolved. In our view, the rally has reduced the margin of safety before Braskem has delivered a credible out-of-court solution, restored working capital access, or addressed the December 2026 standby maturity. That keeps us from turning more constructive, even with yields still elevated across the curve.

We also recognize that the operating backdrop has become less negative since the 4Q25 report. Petrochemical spreads have improved, and management indicated that stronger pricing was already visible in April. Management also noted that current spread levels could support high-cycle EBITDA potential, using 1Q17 as a reference point, when quarterly EBITDA exceeded US$1.0 billion under similar spread conditions. This is an important reference, but not a normalized earnings target. Braskem also emphasized that liquidity, working capital, feedstock access, and utilization remain the binding constraints on translating stronger spreads into cash generation. We therefore view the better spread environment as a meaningful source of optionality, but not yet as confirmation of a durable credit turn.

Keep reading with a 7-day free trial

Subscribe to EM Spreads to keep reading this post and get 7 days of free access to the full post archives.