Braskem Standstill Shifts Focus to Structure

Court protection reduces enforcement risk, but proposed amendment terms make coupon, maturity and recovery structure the key curve drivers

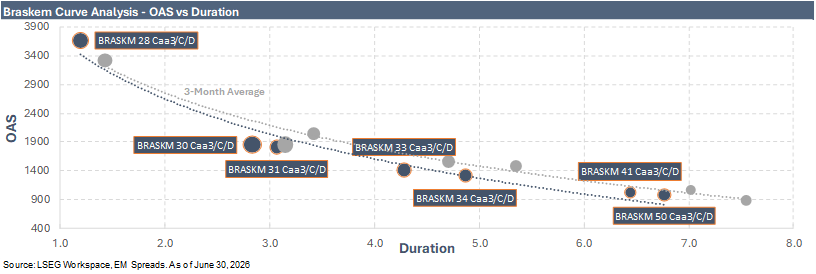

We maintain a Neutral view on Braskem’s senior unsecured complex following the 60-day court stay and rating downgrades. The stay reduces near term enforcement risk, but it does not restore working capital access, solve the maturity wall, or define the final creditor package. This is now a restructuring trade, not a conventional yield trade. Within the curve, we prefer the BRASKM 8.500% 2031s as the best risk adjusted way to stay exposed.

The 2031s offer the best balance of coupon, amended maturity, potential PIK claim accretion and recent trading support. We view the bonds as the preferred curve expression for accounts that want exposure to a negotiated recuperação extrajudicial. The 2034s remain acceptable secondary belly exposure, but we prefer the 2031s because the shorter maturity provides better protection if the restructuring is implemented through a maturity extension rather than a common recovery instrument. The 2028s offer the highest screen yield, but that yield is less meaningful if the maturity is extended. The 2050s offer low dollar price optionality, but under the current proposal they remain very long dated, lower coupon paper. The long end becomes more interesting only if final terms collapse maturities into a common senior unsecured recovery package, which is not the current proposal.

The proposal is more supportive of the higher coupon belly than of the front end or the long end. Braskem is proposing a uniform amendment, not an exchange into a single common takeback instrument: a five-year extension, PIK option through December 2028 and a 200 bps coupon reduction, while preserving principal and unsecured status. That keeps each bond’s original coupon and maturity profile relevant. After the proposed coupon cut, the 2031s would still accrue at roughly 6.50%, versus 2.50% for the 2028s and 2030s and 3.875% for the 2050s. If coupons are PIKed, the higher coupon bonds build a larger accreted claim, while the five-year extension erodes the 2028s’ maturity advantage and leaves the 2050s as very long dated, lower coupon paper.