Cemex 1Q26: Mexico Recovery and Cost Savings Drive EBITDA Beat

Pricing, operating leverage, and structural efficiencies support stronger margins, while U.S. demand and broader volume trends remain mixed

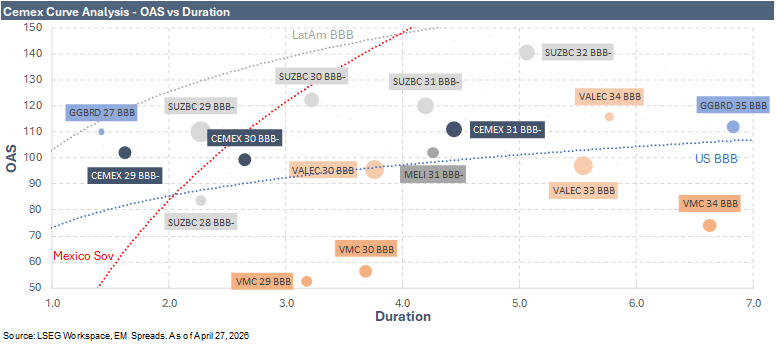

We maintain our Neutral recommendation on Cemex. While 1Q26 results reinforce the constructive credit trajectory we have flagged in prior reports, with operating momentum, margin expansion, and improving underlying cash generation supporting the path toward management’s leverage targets, valuation remains the binding constraint on our stance. Cemex bonds have compressed further across the curve and now trade inside their respective 3 month and 1 year averages, leaving limited room for additional tightening absent a clearer catalyst. In this context, we think the credit remains a high quality hold rather than a fresh Overweight opportunity, with curve selection becoming more important as spreads approach tighter levels. We view the 2029s as the defensive hold and the 2031s as the preferred risk adjusted bond for investors willing to add moderate duration.

From a fundamental standpoint, we view the credit profile as resilient and on a constructive trajectory, supported by structural margin gains under Project Cutting Edge, pricing discipline, and Mexico’s volume recovery. Fitch’s outlook revision to positive from stable on the BBB- rating during the quarter reinforces the rating upgrade path, with management guiding net leverage to converge toward the 1.5x BBB threshold by year end and potential agency action as early as 1H27. Mexico specific risks, trade uncertainty between the U.S. and Mexico, and broader geopolitical volatility remain potential sources of weakness, particularly in a risk off environment.

In our view, neither an Overweight nor an Underweight stance is appropriate at current levels. We do not see a strong enough catalyst for an Overweight, as the path toward a formal upgrade to BBB flat remains more likely skewed to 1H27 and the bonds already reflect much of the improvement. The 2031s trade at 129 bps OAS, broadly in line with the EM Corporate BBB Index at 132 bps OAS and inside their 1 year average, while the 2030s trade 26 bps tight to the EM Corporate BBB Index. At the same time, we do not view an Underweight as warranted given the absence of fundamental deterioration, the supportive rating trajectory, and the company’s improving free cash flow capacity. In our view, the credit story remains intact, but valuation already reflects the improving trajectory, leaving the risk reward more balanced than directional.

Keep reading with a 7-day free trial

Subscribe to EM Spreads to keep reading this post and get 7 days of free access to the full post archives.