CSN 1Q26: Bridge Loan Supports a Show-Me Credit

Wide spreads compensate for execution risk, while deleveraging still depends on asset sales, refinancing, and stronger cash generation

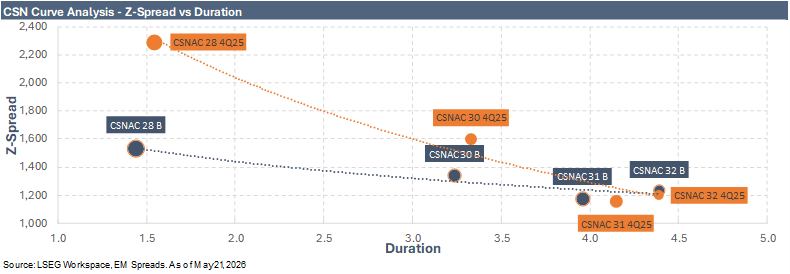

We maintain our Opportunistic Overweight recommendation on CSN, with a preference for the CSN 4.625% 2031s as the more balanced expression and the CSN 5.875% 2032s as the higher upside expression within our preferred part of the curve. We continue to use the Opportunistic Overweight label deliberately, as the thesis remains driven by valuation dislocation, distressed dollar prices, and potential upside from deleveraging execution rather than by a clean improvement in the underlying credit trajectory. The recent downgrade cycle remains central to the spread dislocation, but we think the market is now pricing CSN closer to a distressed recovery trade than a conventional single B credit.

1Q26 results were not strong enough to remove the core concerns around leverage, free cash flow, secured debt, and execution risk, but they also did not point to a near term liquidity event. Revenues declined 7.0% QoQ and 2.8% YoY to R$10.60 billion, while adjusted EBITDA declined 12.1% QoQ on our normalized basis but increased 5.5% YoY to R$2.65 billion. Operating performance was mixed, with weaker sequential EBITDA mainly reflecting mining seasonality, heavier rainfall, and logistics pressure, while cement delivered record EBITDA and steel showed signs of improvement in March and April. Credit metrics improved sequentially, with gross leverage declining to 4.74x from 4.98x and net leverage improving to 3.49x from 3.59x. However, leverage remains materially higher when customer prepayments are included, with gross leverage at 5.98x and net leverage at 4.72x, reinforcing that the balance sheet remains stretched despite the sequential improvement. Cash generation also remained weak, as adjusted EBITDA covered capex and interest, but working capital and other below the line items pushed net free cash flow to a R$1.04 billion outflow. In our view, the quarter keeps the thesis tied to execution, with deleveraging still dependent on stronger cash conversion, inventory reduction, refinancing execution, and asset sale proceeds.

Liquidity remains adequate at the consolidated level, but the headline cash balance deserves caution from a bondholder perspective. CSN’s reported cash of R$14.62 billion covered short term debt by 1.6x as of March 2026, while the standalone parent balance sheet showed a materially tighter position. Parent level cash and short term investments totaled R$2.21 billion against R$4.96 billion of standalone short term borrowings and R$12 million of lease liabilities, leaving a funding gap of roughly R$2.76 billion before refinancing, intercompany flows, asset sales, or new funding sources. We think this distinction matters because the parent company carries the key refinancing burden, including near term bank maturities, financial expenses, capex needs, and the 2028 bond maturity.

The US$1.2 billion bridge loan signed in April, with potential expansion to US$1.4 billion, materially improves near term funding visibility. Including the bridge loan proceeds, pro forma liquidity would increase to approximately R$20.88 billion, short term debt would represent 44.5% of pro forma liquidity, and pro forma liquidity would cover short term debt by 2.2x. We would still not characterize liquidity as strong, given negative free cash flow and the much tighter standalone parent position, but the bridge loan reduces near term refinancing pressure and gives CSN additional time to execute its deleveraging plan.

Keep reading with a 7-day free trial

Subscribe to EM Spreads to keep reading this post and get 7 days of free access to the full post archives.