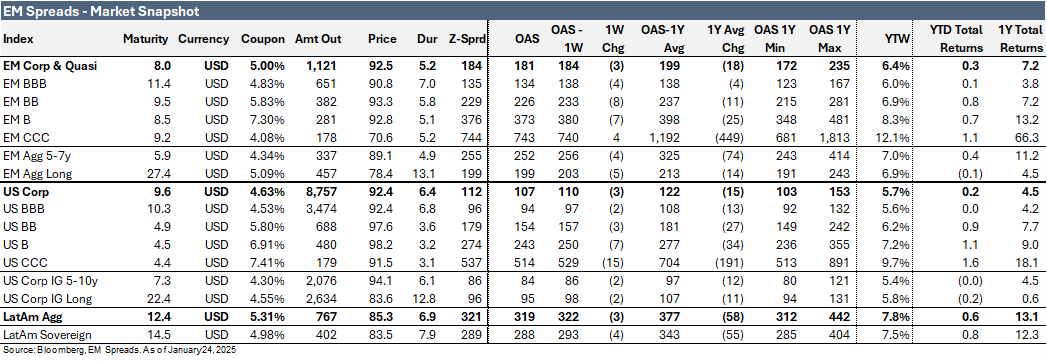

Market Snapshot

The LatAm Corporate Index tightened by 3 basis points (bps) to 319 bps in the week ending on Friday, January 24, 2025. Meanwhile, both the broader Emerging Market (EM) Index and the US Index narrowed by 3 bps to 181 bps and 107 bps, respectively. The region's equity markets showed positive weekly performance: Argentina's Merval Index improved by 4.5%, Brazil's Ibovespa Index rose modestly by 0.1%, Mexico's Mexbol Index increased by 2.2%, and the S&P 500 Index gained 1.8%.

In commodity markets, WTI and Brent crude oil prices traded at US$77.9 per barrel (-4.3% weekly) and US$74.3 per barrel (-3.6%), respectively.

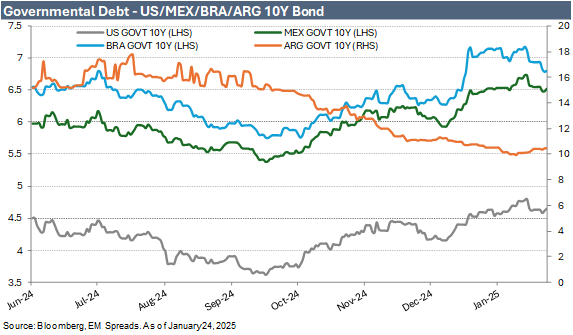

Turning to bond yields, U.S. Treasuries saw modest increases, with the 10-year yield up 2 bps to 4.64% and the 5-year yield also up 2 bps to 4.45%. In contrast, the yield on the 10-year Mexican government bond fell by 3 bps to 6.52%, the 10-year Brazilian government bond decreased by 13 bps to 6.80%, and the 10-year Argentine government bond increased by 5 bps to 10.50% over the week.

Argentina's economic activity in November 2024 returned to pre-Milei levels, marking a full recovery from the initial impact of his fiscal and regulatory overhaul. Economic activity rose by 0.9% from the previous month, surpassing consensus market expectations of 0.4%. The mining and financial intermediation sectors were the strongest performers, growing by 7.1% and 9.9% YoY, respectively. However, in contrast, 10 out of 15 surveyed sectors remained below their levels from a year ago. The construction sector was the biggest laggard, contracting by 14.2% as public spending cuts impacted infrastructure projects. Manufacturing and retail also faced challenges, declining by 2.3% and 1.3%, respectively, which reflects weak domestic demand.

Weekly News

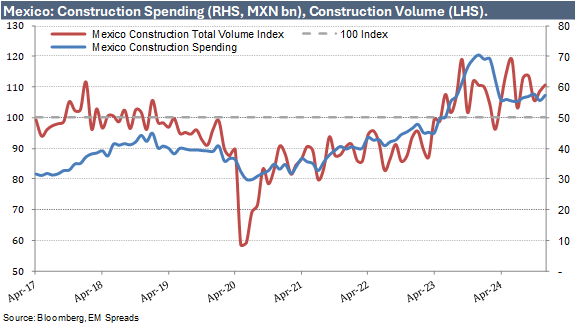

1. Cemex – Mexico Construction Key Indicators

Fundamentals in Mexico remained relatively healthy in October and November compared to historical figures, though they came under significant pressure relative to the same period in 2023. Mexican construction spending declined by 19.5% YoY in October and 18.7% in November. On a month-over-month basis, the construction spending index fell 3.6% in October but rebounded 3.0% in November.

We see a slower construction pace as the new government establishes its agenda and implements policy changes, alongside geopolitical uncertainty surrounding Trump's second presidency and its policies toward Mexico. In September 2024, the Mexican construction business confidence index fell below 50, signaling a contraction at 48, only improving to 49 in both October and November. Meanwhile, the Mexican construction activity index remained in expansion territory, above 100, at 109 in October and 111 in November, though significantly below the 119 recorded in May 2024.

Regarding macroeconomic indicators, Mexico's GDP per capita is projected to experience modest growth, with an increase of 1.5% in 2024, followed by 1.1% in 2025, and then rising to 1.8% in 2026. There is considerable uncertainty surrounding the new Trump presidency's trade and immigration policies, which could exert significant pressure on Mexico's economy, especially as these policies will take time to implement. This uncertainty will likely curb investment and growth in 2025 while it persists. Unemployment is expected to rise modestly from 2.8% in 2024 to 3.3% in 2025, slightly decreasing to 3.2% in 2026. Meanwhile, the fiscal deficit is anticipated to be substantial at -5.4% of GDP in 2024, improving to -3.8% in 2025 and further to -3.4% in 2026.

Looking forward, construction in Mexico is set to be slower than previously expected in the early months of 2025; however, robust spending on infrastructure and housing is anticipated to improve, supported by nearshoring and the increasing demand for infrastructure in the US, where only a portion of the Infrastructure Investment and Jobs Act (IIJA) funding has been allocated. Mexico's new government agenda, which emphasizes housing and infrastructure, should benefit Cemex as a leading global cement producer and a dominant player in the profitable Mexican market. The government has announced plans to build 1 million homes over the next six years and to develop ten economic corridors nationwide to capitalize on nearshoring opportunities.

Credit View

We continue to view Cemex as an attractive emerging market credit story but now have a Market Perform recommendation. Macroeconomic uncertainties in Mexico, including a recently elected nationalistic administration, a significant fiscal deficit, GDP growth below 2%, dependency on uncertain US-Mexico relations, and foreign exchange risk, add pressure to the credit story. We believe that initially perceived as unfavorable for US-Mexico relations, Trump's second presidency significantly increases the headline risk for the notes, thereby limiting the potential for outperformance.

2. Cemex Knoxville Cement Plant Selected for DOE-Funded Carbon Capture Test Center

On January 20, 2025, Cemex announced that the U.S. Department of Energy's Office of Fossil Energy and Carbon Management has selected its Knoxville, Tennessee, cement plant for a pioneering carbon capture, removal, and conversion test center. The project is part of a broader initiative distributing $101 million across five sites to develop decarbonization solutions for cement plants and power facilities. Cemex will work on the test center's conceptual design and business structure in Phase 1 in collaboration with the University of Illinois Urbana-Champaign and other cement producers. A competitive selection process in Phase 2 will determine the facility's construction and operation, providing a platform for testing advanced carbon capture technologies.

Cemex's participation aligns with its broader decarbonization strategy, which includes carbon capture, utilization, and storage technologies. The initiative is a key component of its "Future in Action" program, aimed at achieving net-zero carbon emissions by 2050.

3. YPF/Vista - Shale Boom Drives Argentina’s Energy Trade Surplus

On January 21, 2025, the Argentine government announced that Argentina recorded a $5.7 billion energy trade surplus in 2024, the widest in 18 years, driven by increased oil and gas production from the Vaca Muerta shale formation. According to Argentina's Energy Department, pipeline expansions have boosted crude exports while reducing natural gas imports, contributing to the positive balance. In December, Argentina recorded an energy trade surplus of $852 million, driven by a significant increase in exports and a notable reduction in imports. Throughout 2024, fuel and energy exports grew by 22.3%, reaching $9.7 billion, which accounted for 12.1% of Argentina's total exports. Chile was the primary destination for these exports, with $2.8 billion, a 74.1% increase from 2023. Conversely, imports of fuel and lubricants decreased by 49.4% YoY, totaling $4.0 billion.

Expectations are for the surplus to grow in 2025, reinforcing a structural shift toward higher energy exports and lower imports. This trend supports President Milei's efforts to build foreign reserves, a crucial step toward lifting capital controls that could support foreign investment.

Credit View

For both Vista and YPF, we believe that improving Argentine macroeconomic conditions will likely support these companies, bolstered by the energy sector's pivotal role in the positive national narrative. Both companies are leading shale oil producers in Argentina and are well-positioned to capitalize on the vast potential of the Vaca Muerta formation, one of the largest shale plays outside North America. This formation holds the potential for significantly increasing national energy exports, expected to lead to higher foreign currency inflows, which is particularly beneficial in an environment focused on currency stabilization efforts.

4. YPF Signs MoU with Indian Firms for LNG Exports

On January 22, 2025, YPF announced that it signed a memorandum of understanding (MoU) with three Indian firms to explore the potential export of up to 10 million tonnes per year of LNG. YPF CEO Horacio Marín signed the agreement in New Delhi with executives from Oil and Natural Gas Corporation, Gas Authority of India Ltd, and ONGC Videsh Ltd. The CEO emphasized Argentina’s ambition to become a key energy exporter, targeting US$30 billion in revenues over the next decade.

Beyond LNG exports, the MoU includes cooperation in lithium, critical minerals, and hydrocarbon exploration and production. Marín has been actively seeking LNG buyers for gas from Vaca Muerta, the world's second-largest shale gas reserve, with visits to Israel, South Korea, and Japan. This agreement aligns with President Javier Milei’s efforts to attract foreign investment and boost export revenues. However, its success will depend on securing financing for critical infrastructure and maintaining stable production amid Argentina's economic challenges.

Credit Impact – Long-term positive

The news aligns with YPF’s Vaca Muerta opportunity as the company prioritizes developing this major shale formation to expand shale oil and gas production, which could account for 80% of its output by the end of the decade. YPF’s divestment strategy enables it to focus on more profitable shale assets, improving overall profitability by reducing production costs. Additionally, the company is making substantial investments in infrastructure to accelerate shale development and capitalize on the growing global demand for affordable, reliable, and sustainable energy. This positions YPF as a key net exporter of crude oil and LNG. However, the company’s LNG project will require significant investment over the next decade, which could strain free cash flow generation in the coming years and, in turn, weigh on YPF’s overall credit profile.

5. Fitch Affirms YPF's Ratings at 'CCC'

On January 22, 2025, Fitch Ratings has affirmed YPF S.A.'s Long-Term Foreign and Local Currency Issuer Default Ratings (IDRs) at 'CCC', reflecting its strong government ties, financial stability, and strategic importance to Argentina. YPF’s senior unsecured notes remain rated 'CCC' with a Recovery Rating of 'RR4', while its Standalone Credit Profile (SCP) is 'b'.

Fitch’s Key Factors:

YPF maintains a close relationship with the Argentine government, which owns 51% of the company and influences its pricing policies and strategic decisions. The company holds a 57% market share in Argentina’s gasoline and diesel market, reinforcing its critical role in the energy sector. Production is expected to average 600,000 barrels of oil equivalent per day (boed), with costs projected to decline in 2024 and 2025 due to efficiencies from unconventional production. Financially, YPF’s leverage is improving, with total debt/EBITDA expected to decrease from 1.8x in 2023 to below 1.0x over the rating horizon. However, macroeconomic headwinds persist, including capital controls and restricted access to international funding.

YPF's operational scale is smaller than Petrobras and PEMEX but comparable to Ecopetrol. While its leverage remains stable, the company continues to face a high cost of capital due to Argentina's economic volatility. Unlike ENAP and Petroperú, YPF is an integrated energy company, providing greater financial flexibility. YPF's strategic importance in Argentina’s energy sector remains strong, but its credit profile remains vulnerable to economic and policy uncertainties.

6. Pemex Shuts Dos Bocas Refinery Due to Crude Quality Issues

On January 23, 2025, it was reported that Pemex had shut down its Dos Bocas refinery, also known as Olmeca, due to high salt content in its crude oil supply, which can damage equipment and disrupt operations. The refinery, designed to process 340,000 barrels per day of heavy sour Maya crude, has faced persistent challenges since its inauguration in July 2022. These issues include delays in reaching operational capacity, technical problems, and financial constraints. The refinery was intended to be a cornerstone of Mexico's strategy to achieve energy independence by processing heavy sour crude domestically but has struggled to perform as expected. This latest shutdown underscores ongoing operational inefficiencies and the complexities of refining Mexico's heavy, sulfur-rich crude.

The shutdown implies that Mexico will likely increase its reliance on imported gasoline and diesel, at least temporarily, as the refinery was supposed to reduce this dependency. This could lead to a spike in fuel import costs, putting additional pressure on Pemex's already strained financials. This development also coincides with Pemex's efforts to address its US$20 billion debt to suppliers, with plans to clear payments by March. Dos Bocas has struggled to reach full capacity, consistently operating below expectations. Pemex has not yet commented on the refinery’s status.

EM Spreads’ Most Recent Publications:

YPF (January 8, 2025): Recommendation on YPF's new USD 9NC4 unsecured notes.

Vista Energy (December 18, 2024): New issue snapshot.

YPF (December 3, 2024): Initiation coverage report.

Disclaimer

Opinions presented in this report are based on and derived primarily from public information that EM Spreads LLC ("EM Spreads," "We," or "Our") considers reliable. Still, we make no representations or warranty regarding their accuracy or completeness. EM Spreads accepts no liability arising from this report. No warranty, express or implied, as to the accuracy, timeliness, completeness, or fitness for any particular purpose of any such analysis or other opinion or information is given or made by EM Spreads in any form.

All information contained in this document is protected by Copyright law, and none of such information may be copied, repackaged, transferred, redistributed, resold, or stored for subsequent use for any such purpose, in whole or in part, by any person without EM Spreads’ prior written consent. All rights reserved. Reproduction of this report, even for internal distribution, is strictly prohibited. The content shall not be used for any unlawful or unauthorized purposes.

This content is provided on an "as is" basis and should not be regarded as a substitute for obtaining independent advice. EM Spreads disclaims all express or implied warranties, including, but not limited to, any warranties of merchantability or fitness for a particular purpose or use, freedom from bugs, software errors, or defects, that the content’s functioning will be uninterrupted or that the content will operate with any software or hardware configuration. Investors must determine the appropriateness of an investment in any instruments referred to herein based on the merits and risks involved, their own investment strategy, and their legal, fiscal, and financial position. As this document is for information purposes only and does not constitute or qualify as an investment recommendation or advice or as a direct investment recommendation or advice, neither this document nor any part of it shall form the basis of or be relied on in connection with or act as an inducement to enter, any contract or commitment whatsoever. Nothing in this report constitutes investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise a personal recommendation to you.

The opinion contained in this report may not be suitable for your specific situation. Investors are urged to contact their investment advisors for individual explanations and advice. EM Spreads does not offer advice on the tax consequences of investments, and investors are urged to contact an independent tax adviser for individual explanations and advice. In no event shall EM Spreads be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special, or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of this report.

This document may contain forward-looking statements that involve risks and uncertainties. Actual results may differ materially from those expressed or implied in such statements. EM Spreads undertakes no obligation to update any forward-looking statements to reflect events or circumstances after the date of this document or to discontinue it altogether without notice. EM Spreads reserves the right to modify the views expressed herein without notice.

The content in this report is provided to you for information purposes only. EM Spreads’ opinions and analysis are not recommendations to purchase, hold, or sell any securities or to make any investment decisions and do not address the suitability of any security. EM Spreads assumes no obligation to update the content following publication in any form or format. The content in the report shall not be relied on and is not a substitute for the skill, judgment, and experience of the user, its management, employees, advisors, and /or clients when making investment and other business decisions. EM Spreads has not taken steps to ensure that the securities referred to in this report are suitable for any investor.

This report is not directed to or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any locality, state, country, or other jurisdiction where such distribution, publication, availability, or use would be contrary to law or regulation or which would subject EM Spreads to any registration or licensing requirement within such jurisdiction. No person should review or rely on this report if such review or reliance would require EM Spreads to obtain any registration or license in any such jurisdiction.

All estimates and opinions expressed in this report reflect the analysts' independent judgment as of the issue's date about the subject company or companies and its or their securities. No part of the analyst's compensation was, is, or will be directly or indirectly related to this report's specific recommendations or views. The research analysts contributing to the report may not be registered /qualified as research analysts with any regulatory or government body or market regulator.