Gerdau 4Q25: North America Drives Earnings, Brazil Margins Remain Pressured

73% EBITDA from U.S. operations supports stability, while import penetration and trade defense timing weigh on Brazil recovery

We maintain our Neutral recommendation on Gerdau. We continue to view the company as a solid BBB credit with a conservative balance sheet, strong liquidity, and a structurally advantaged North American footprint. However, at current spread levels, we see limited scope for material re-rating, particularly as Brazil remains challenged by persistent import penetration and only incremental progress on trade-defense measures.

From a business-risk perspective, 4Q25 reinforced the structural divergence within the portfolio. North America, which accounted for 73% of consolidated adjusted EBITDA in the quarter, continues to benefit from Section 232 protection, resilient non-residential construction demand, data center and renewable energy investment, and a supportive backlog. By contrast, margins in Brazil remain pressured, with import penetration at 21% and EBITDA margins in the high single digits. While Miguel Burnier should structurally enhance Brazilian cost competitiveness from 1H26 onward, we think the timing and magnitude of margin normalization remain contingent on effective trade enforcement and domestic pricing dynamics.

Financially, leverage at 0.91x net and 1.55x gross remains conservative, with FFO to debt at 47.3% and liquidity covering maturities through 2035. The reduction in 2026 capex to R$4.7 billion should support a clearer free cash flow inflection, but shareholder distributions and buybacks limit the scope for materially lower leverage in the near term. As a result, we view the credit as stable and resilient, but without a clear catalyst for meaningful spread tightening from current levels.

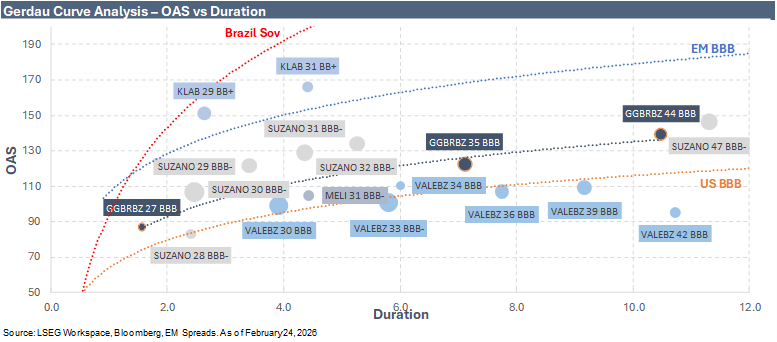

At current levels, Gerdau’s curve appears broadly aligned with LatAm BBB comparables, offering limited incremental compensation for extending duration beyond the belly.