JBS 4Q25: Diversification Supports Better Than Expected Results

Brazil and Australia offset weaker protein margins, while U.S. beef and poultry still came in above expectations

We maintain our Overweight recommendation on JBS, as 4Q25 results continue to support a constructive credit view despite some sequential pressure on profitability. The main strength of the story remains the scale and diversification of JBS’s global protein platform, which continues to offset weaker conditions in businesses facing more challenging livestock and commodity dynamics. This was again evident in 4Q25, as stronger performances in Brazil, Australia, and poultry helped balance weaker results in North America Beef and pork. The company also ended the quarter with strong liquidity, solid free cash flow, and net leverage of 2.68x, comfortably within management’s 2x to 3x target and supportive of investment-grade metrics. While we continue to view North America Beef as the main operating overhang into 2026, we think JBS’s diversified earnings base and healthy cash generation keep the overall credit story well anchored.

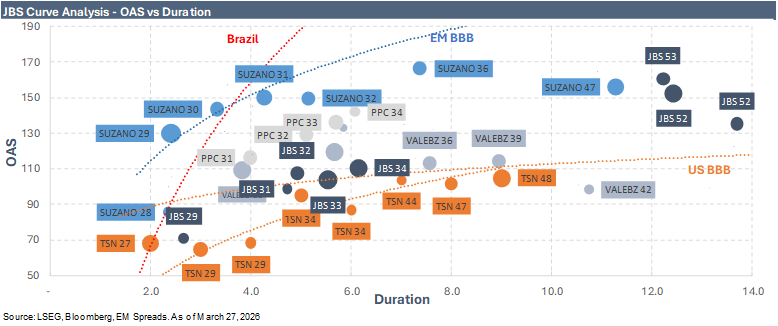

Within the curve, we continue to see the best value concentrated in the long end. We favor the JBS 7.250% 2053s from a carry-to-duration standpoint, as they offer a 6.5% YTW at 158 bps OAS, a price of $109.3, and 12.2 years of duration. Relative to Tyson, that implies 53 bps of incremental spread versus TSN’s 5.100% 2048s at 105 bps OAS and 56 bps versus TSN’s 4.550% 2047s at 102 bps, with broadly comparable duration. The 2053s also trade 53 bps wide to the U.S. Corp Long benchmark at 105 bps OAS, although we view that comparison more as a technical reference given the materially higher quality of that index. While that pickup has narrowed modestly from the roughly 60 bps differential implied by 3-month average spreads, we think the long end has retained more of its relative value than the belly, where compression versus Tyson and broader BBB benchmarks has been more pronounced. We also like the JBS 4.375% 2052s, which yield 6.3% at a price of $75.4 and 134 bps OAS. While the 2052s carry modestly higher duration than the 2053s and trade at a lower OAS, the $75.4 price embeds meaningful pull-to-par and convexity that we think compensate for the additional duration. In our view, the discount price offers better pull-to-par and somewhat better protection if spreads widen, while the 2053s provide stronger carry. The JBS 6.500% 2052s at $100.6 also remains a reasonable near-par alternative in the long end, but we continue to see the clearest value in the 2052s and 2053s.

In the belly, the JBS 6.750% 2034s remain the most interesting intermediate bond, but at 110 bps OAS they now trade well inside their 3-month average of 153 bps and their 1-year average of 123 bps, suggesting valuations have tightened materially and that upside is more limited from current levels. They are also only 15 bps wide to Tyson’s 5.700% 2034s at 95 bps OAS and 23 bps wide to Tyson’s 4.875% 2034s at 87 bps, which reinforces our view that the belly now looks closer to fair value. More broadly, the 2034s are only modestly wide to the U.S. BBB benchmark at 107 bps OAS and are tight to the EM BBB benchmark at 122 bps, while the JBS 5.950% 2035s at 119 bps OAS still offer somewhat better relative value in that part of the curve. That said, management’s comments around potential liability management involving the 2033 and 2034 bonds provide an additional technical element worth monitoring, as those bonds carry coupons of 5.750% and 6.750%, respectively, above what JBS could likely issue today in long-dated maturities.

We remain Neutral on the short end. The 2029s yield 4.7% for 2.7 years of duration and trade at 71 bps OAS, leaving them only 3 to 6 bps wide to Tyson’s 2029s, which in our view is not enough pickup to make the short end particularly compelling.

Keep reading with a 7-day free trial

Subscribe to EM Spreads to keep reading this post and get 7 days of free access to the full post archives.