MercadoLibre 1Q26: Full Cart, Thinner Margins

Ecosystem growth remains impressive, but credit expansion, investment intensity, and fair valuation keep bond upside limited

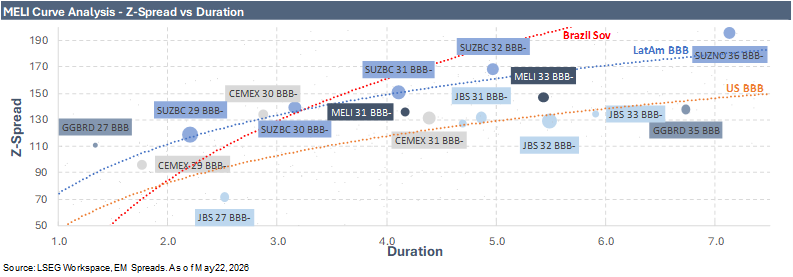

We maintain our Neutral recommendation on MercadoLibre. We continue to view MELI as one of the highest-quality BBB credits in LatAm, supported by structural leadership in e-commerce and fintech, strong ecosystem dynamics, scale advantages, and robust operating cash generation. However, 1Q26 reinforced the same credit trade-off that shaped our 4Q25 view. Growth remains exceptional, but management continues to prioritize ecosystem expansion, credit growth, free shipping, fulfillment, 1P, cross-border trade, AI, and credit card scaling over near-term margin recovery. We view this strategy as supportive of long-term franchise value, but it keeps profitability under pressure, sustains a structurally larger balance sheet, and limits the case for a more constructive bond recommendation at current spreads.

From a credit perspective, the quarter does not change our view of MELI as a strong investment-grade issuer, but it reinforces why we remain Neutral. The company continues to generate substantial operating cash flow, but adjusted free cash flow remains sensitive to the pace of Mercado Pago credit growth. Leverage moved higher, liquidity coverage tightened, and margin recovery is likely to remain gradual as management keeps investing behind ecosystem growth. We do not view these trends as a material credit concern given MELI’s scale, cash generation, and market access, but they temper the case for adding exposure despite the modest spread give-back and better all-in yield.