MercadoLibre 4Q25: Strong Growth, Margin Pressure Persists

Neutral as ecosystem investments and credit expansion weigh on profitability and limit near-term spread compression

We maintain our Neutral recommendation on MercadoLibre. We continue to view MELI as one of the highest-quality BBB credits in LatAm, supported by structural leadership in e-commerce and fintech, strong ecosystem dynamics, and solid internal cash generation. However, at current spread levels, we see limited scope for further material spread compression. While the credit profile remains sound, near-term margin pressure and structurally higher funding needs tied to credit growth limit the case for a re-rating.

The 4Q25 results reinforced robust growth across Commerce and Fintech, but also confirmed that management remains focused on ecosystem expansion rather than margin optimization. Strategic initiatives in Brazil logistics, first-party operations, cross-border trade, and credit card scaling continue to weigh on profitability in the near term. While we view this as supportive of long-term franchise value, it sustains elevated investment intensity and a structurally higher balance sheet footprint, reflected in higher reported debt and a tighter liquidity coverage profile.

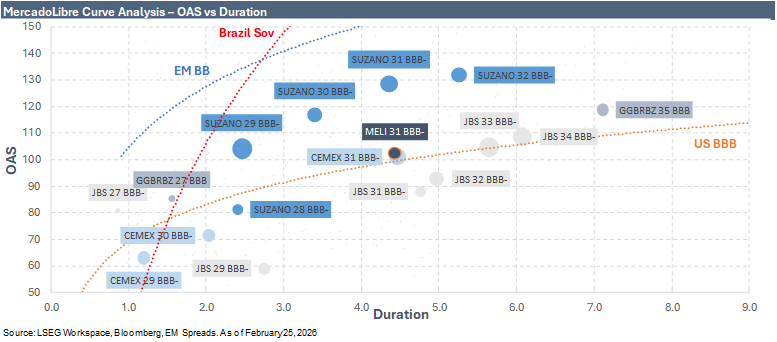

From a relative value perspective, MELI (BBB-) 3.125% 2031 notes trade at approximately 102 bps OAS with 4.4 years of duration and a 4.6% YTW. The bonds are currently priced at $93.4, below par, which provides visible pull-to-par support over time if spreads remain stable. That said, the discount price largely reflects the lower coupon structure rather than an outright spread concession, and convexity benefits are moderate given the intermediate duration profile. At current levels, we think meaningful price upside would primarily require further spread compression.

Versus benchmarks, the 2031s trade through the EM BBB index at 117 bps, implying roughly 15 bps of tightness despite MELI’s meaningful exposure to higher-risk Latin American markets. The bonds also trade through their recent historical averages, with the 3-month average at 134 bps and the one-year average at 126 bps, while remaining above the one-year low of 84 bps. Spread performance versus EM Corp BBB shows that the 2031s have typically traded modestly tight to the index, reinforcing their premium positioning within the asset class.