Minerva 1Q26: Bigger Platform, Same Cattle Cycle Pressure

Scale, pricing, and integration support EBITDA, while cattle costs and working capital needs keep credit improvement gradual

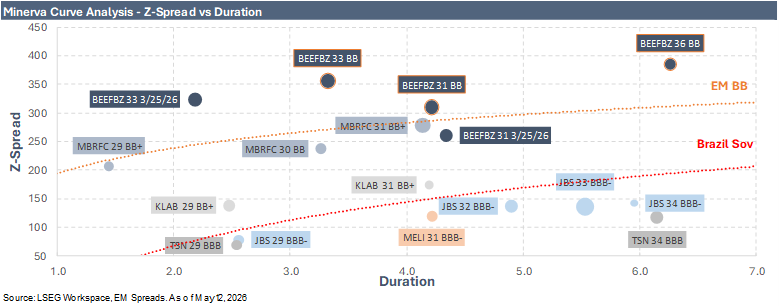

We maintain our Neutral recommendation on Minerva, but with a more constructive valuation tone following the recent widening in the BEEFBZ 4.375% 2031 notes. Our 4Q25 downgrade was anchored on the view that the re-rating had largely played out, with the bonds trading close to or inside relevant EM BB benchmarks and offering limited asymmetry after a strong period of spread compression. Current levels have changed that picture. The 2031s have widened back to a meaningful spread premium versus the EM BB index while retaining a clean below-par structure, providing a more reasonable entry point. At the same time, we do not think the move is enough to restore an Overweight stance, as 1Q26 results still point to a balanced rather than improving operating setup. Revenue and EBITDA remain supported by scale, pricing, geographic diversification, and acquisition integration, but cattle cost inflation continues to pressure margins and free cash flow conversion, while cash interest coverage remains the key constraint to a more constructive credit view.

Minerva’s credit story remains intact. The company delivered 16.2% YoY EBITDA growth in 1Q26, reduced gross debt by 11.4% QoQ through active liability management, and maintained R$10.88 billion in liquidity, covering short-term maturities by 3.1x. Capital allocation continues to balance deleveraging with a more visible shareholder return framework, while the diversified export platform across Brazil, Argentina, Colombia, Uruguay, Paraguay, and Australia provides flexibility across origins and end markets.

However, the operating backdrop is not without pressure. Management expects 2026 margins to remain below 2025 levels on higher cattle costs across key origins, gross margin contracted YoY in 1Q26, net free cash flow was negative at R$811 million, net leverage increased modestly to 2.77x, and cash interest coverage of 1.93x remains below the 2.0x level we view as necessary for a more constructive stance. We note that cash financial expenses declined YoY in 1Q26, supported by active liability management. The new 7.500% 2036 notes are expected to target the rollover of short-term debt, which should eliminate 2026 refinancing risk and improve Minerva’s maturity profile and refinancing flexibility. While the coupon is meaningful, the net impact on cash interest will depend on the cost and amount of debt ultimately repaid. Sustained EBITDA growth and stronger free cash flow conversion after working capital therefore remain central to further improvement in interest coverage and credit metrics.