PEMEX 1Q26: Policy Support Drives Rally, but Standalone Weakness Persists

Debt reduction and sovereign backing support Overweight, while weak cash generation and tighter spreads require greater bond selectivity

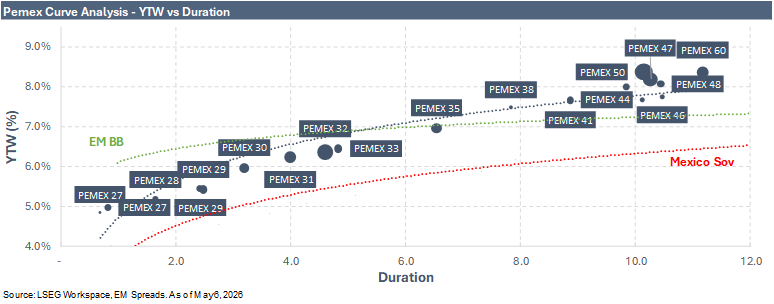

We maintain our Overweight recommendation on PEMEX, while becoming more selective across the curve after the strong policy-driven rally. The 1Q26 results reinforce our core view that PEMEX remains a government-backed credit, with bondholder performance driven more by policy support, liability management, and market access than by a self-sustaining recovery in standalone cash generation. Adjusted EBITDA recovered sharply, debt declined again, and government-related inflows through equity contributions, the FONADIN subvention, and collections from the Mexican government more than covered the company’s pre-contribution cash deficit. The stronger oil and refined product price environment provided an incremental tailwind, although in our view this layered onto rather than reshaped the credit story. For bondholders, we think 1Q26 again showed the depth of government commitment behind the credit.

At the same time, 1Q26 does not remove the structural weakness in PEMEX’s operating model. Adjusted EBITDA recovered to $6.71 billion from a very weak 4Q25 base, but the YoY comparison was less clean in local-currency terms, with EBITDA declining in MXN and consolidated revenues also lower in MXN. Cash generation improved at the headline free cash flow level, but pre-contribution net free cash flow remained negative after working capital, taxes, lease payments, and other cash uses. We would also be careful about extrapolating the lower 1Q26 capex run rate, as investment spending is likely to accelerate through the rest of the year. Liquidity has improved, supported by lower short-term debt, a cash balance that remains above recent historical levels, and meaningful revolver availability. However, the standalone position is not yet comfortable, as short-term debt still represents a high share of total liquidity. We therefore view the quarter as evidence of better liquidity visibility, supported by government backing and market access, rather than a durable improvement in standalone cash generation capacity.

The 2026 setup is more balanced, but also more valuation-sensitive. PEMEX has made visible progress in reducing debt, extending funding visibility, improving bank financing terms, and reentering the local capital markets. The renewal and expected improvement of revolving credit facilities should support liquidity flexibility, while management’s focus on debt-neutral issuance and liability management reduces near-term refinancing pressure. A debt-neutral USD transaction combined with tenders or buybacks would be credit positive, as it would reinforce market access and help smooth the maturity profile, but we would not use that optionality to favor any single short-dated bond at current levels. The cooperation agreement with Petrobras is also directionally positive, particularly as a potential source of technical expertise, operating discipline, and project execution support. However, we would not treat it as a near-term credit catalyst, given the absence of disclosed project economics, investment commitments, implementation timelines, or expected financial contribution.