Pemex 4Q25: Debt Relief Anchors the Credit, Operating Fragility Persists

Liability management operations improve maturity profile and market access, though negative funds from operations and structural production challenges persist

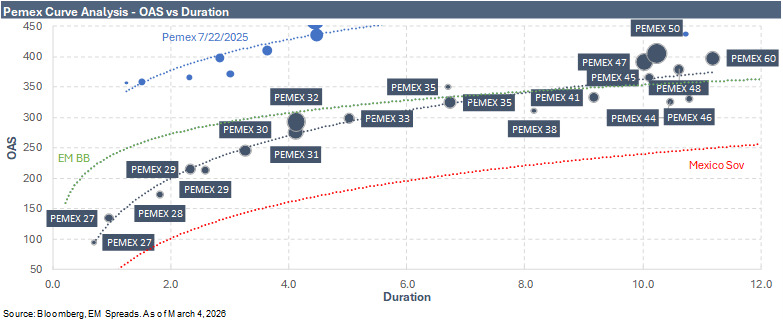

We maintain our Overweight recommendation on Pemex, supported by the continued demonstration of extraordinary sovereign backing and the resulting improvement in the company’s refinancing profile. Mexico’s 2025 debt strategy, including sovereign bond issuance, the $12 billion pre-capitalized securities (P-Caps) transaction, and the $9.9 billion bond buyback, has materially reduced Pemex’s financial debt and shifted part of the refinancing burden onto the sovereign balance sheet. These measures have strengthened liquidity visibility and improved the company’s maturity profile, reinforcing the sovereign’s commitment to supporting the company and anchoring near-term credit performance.

At the same time, 4Q25 results highlight the structural fragility of Pemex’s operating model. Revenues declined sequentially amid weaker crude realizations and a sharp contraction in export volumes, while adjusted EBITDA decreased to $1.85 billion from $3.20 billion in 3Q25. Free cash flow before working capital remained deeply negative, as operating cash generation was insufficient to cover elevated capital expenditures and interest payments. While recent liability management operations have helped reduce gross financial debt and improve leverage metrics, funds from operations remained negative, underscoring the company’s continued dependence on government support to stabilize liquidity and sustain investment.

Looking ahead, the 2026 credit story appears more dependent on technical and policy factors than on a meaningful improvement in underlying operating fundamentals. The large-scale support measures implemented during 2025 materially reduced near-term refinancing risk, but the scope for additional extraordinary interventions appears more limited in the near term. As a result, we believe the next phase of performance will likely depend more heavily on the pace of sovereign support through the federal budget, the evolution of Pemex’s funding strategy, and broader EM credit market conditions.

Keep reading with a 7-day free trial

Subscribe to EM Spreads to keep reading this post and get 7 days of free access to the full post archives.