Simpar 1Q26: Improving Margins, Harder Upside

Lower capex and stronger EBITDA support the credit direction, while tighter spreads raise the bar for recurring FCF and deleveraging

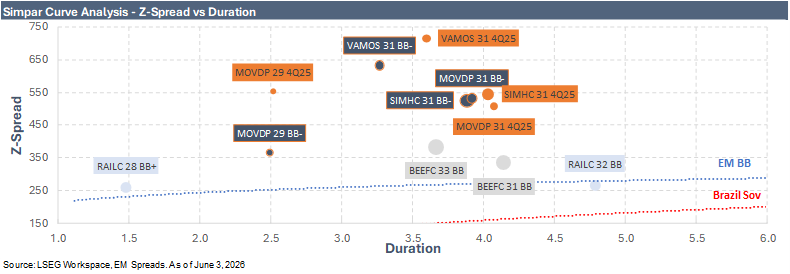

We move Simpar to Neutral at the issuer level, while expressing our constructive view through an Overweight recommendation on the MOVIBZ 5.250% 2031 notes as the preferred total-return and relative-value opportunity within the bond curve. The credit story is improving directionally, but after the recent spread compression, the 1Q26 results were not clean enough to support a broad Overweight recommendation across the group at current bond levels. Leverage remains elevated, interest coverage remains thin against Brazil’s high interest rate backdrop, and reported net free cash flow remained negative in 1Q26 after working capital. The lower-capex and value-extraction phase is becoming more visible, but the deleveraging thesis still needs cleaner evidence of recurring free cash flow after interest and working capital, with less reliance on temporary working capital swings, asset monetization, capital increases, or continued refinancing access.

The recommendation is therefore less about a broad re-rating call and more about where the next leg of risk-adjusted upside remains. Simpar’s operating direction supports staying involved in the credit, but the first stage of spread compression across parts of the curve has largely played out. VAMOBZ 2031 remains the most carry-efficient bond in the 2031 area, but at 588 bps it now trades close to its 1Y Z-spread minimum of 583 bps. By contrast, MOVIBZ 2031 offers the cleaner total-return setup, as it combines a deep discount price, operating-company recourse, and a current 529 bps Z-spread.