Simpar 4Q25: Better Execution, but Cash Generation Remains Mixed

Consolidated margins improved, though the quarter remained investment-heavy and cash flow was supported by working capital and the Ciclus Rio sale.

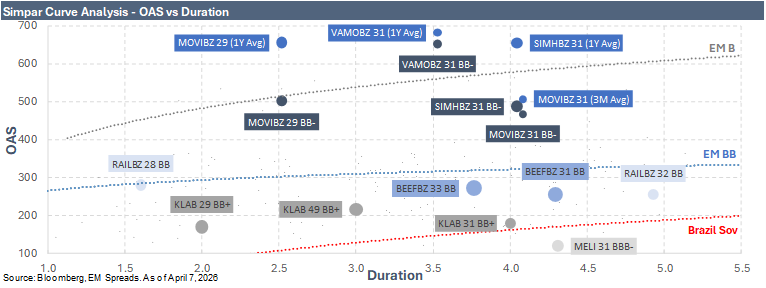

We maintain our preference for the VAMOBZ 9.200% 2031 notes as the primary expression of a constructive view on the credit. Since January 6, SIMHBZ 2031 has compressed by roughly 148 bps to 498 bps, while VAMOBZ 2031 has drifted modestly wider to 649 bps, creating a 151 bps spread gap versus the essentially flat relationship that existed at initiation and a 160 bps yield gap in VAMOBZ’s favor. VAMOBZ also retains a shorter duration at 3.5 years versus 4.0 years for SIMHBZ. In our view, this combination of higher carry, lower duration, and operating-company positioning continues to make VAMOBZ the most attractive way to express the improving Simpar credit story for investors focused on defensive carry and downside protection. MOVIBZ 2029 remains the middle ground for investors focused on shorter duration and liquidity.

The 4Q25 results validate the directional thesis we outlined at initiation. Operating performance improved meaningfully, leverage continued to decline, and capital intensity reached its lowest level in five years, supporting the view that the group has entered a lower-investment and potentially more cash-generative phase. That said, underlying free cash flow remains dependent on working capital support and asset monetization rather than recurring operations alone, while Brazil’s elevated interest rate environment continues to constrain deleveraging by absorbing a large share of EBITDA and keeping EBITDA interest coverage thin. Liquidity is adequate, capital markets access has remained open at improving cost levels, and management has framed 2026 as a value-extraction and efficiency phase, with cash generation expected to become more resilient as investment needs normalize.

Within the group, cash conversion trends also reinforce our preference for Vamos. The comparison is directional rather than fully comparable, but it remains informative. In 4Q25, Vamos generated EBITDA equal to 3.8x net capex, versus only 0.6x at Movida, highlighting that Vamos is already operating in a much clearer lower-investment and higher-cash-conversion phase, while Movida remains materially more capital intensive. Simpar sits in between at the consolidated level, but the ratio is closer to 1.1x when using adjusted EBITDA rather than reported EBITDA, which benefited from the Ciclus Rio divestment. We think this reinforces the view that the strongest internal cash-generation profile in the complex currently sits at Vamos.