Suzano 1Q25: Credit Metrics Improve Despite EBITDA Miss, Remain Outperform

Higher Costs Weigh on Margins, but Credit Profile Strengthens with Lower Net Leverage, Strong Liquidity, and a Firm Commitment to Prudent Capital Allocation

Key Insights and Recommendations

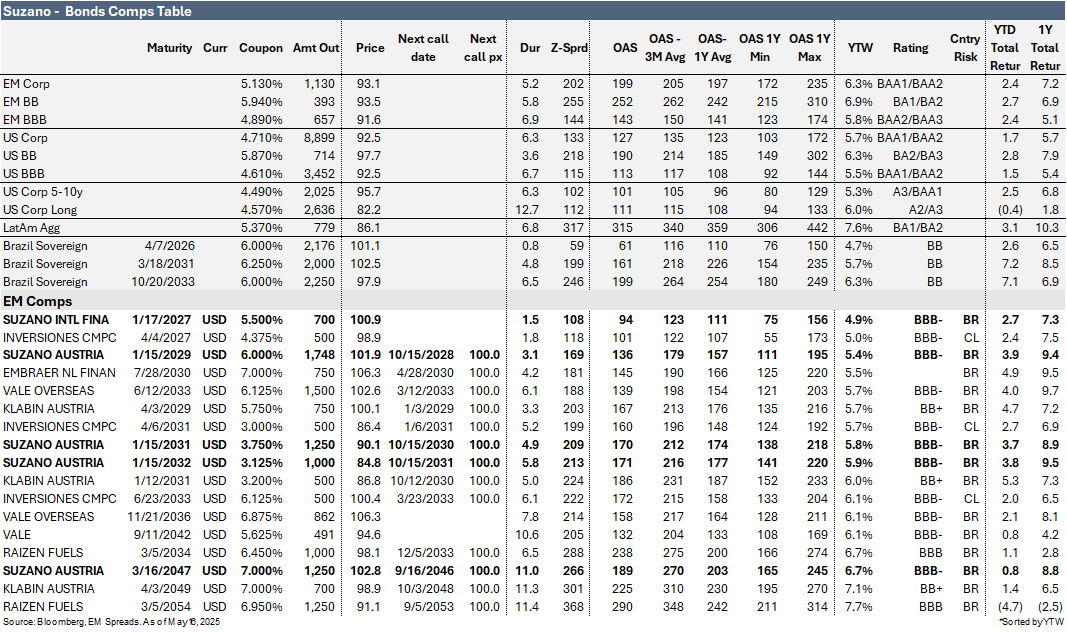

We maintain our Outperform recommendation on Suzano’s 2031s and 2032s, while keeping the rest of the curve at Market Perform.

Suzano delivered weak 1Q25 results with EBITDA margin contraction driven by higher costs. The company generated revenues of R$11.55 billion, reflecting an 18.5% sequential decline but a 22.1% YoY increase, missing market consensus by 3.6%. Pulp revenues decreased 23.1% QoQ but increased 17.0% YoY, while Paper revenues declined 1.3% sequentially but improved 40.1% YoY. The sequential deterioration was primarily caused by an 18.1% decrease in sales volumes to 3,041kt, with Pulp sales volume down 19.3% and Paper sales volume down 9.4%, largely due to seasonal factors and strategic inventory rebuilding. Average prices declined 0.5% QoQ, with Pulp prices down 4.7%, reflecting the invoicing of backlogs at lower price levels, partially offset by an 8.9% increase in Paper average prices.

Adjusted EBITDA was R$4.87 billion in 1Q25, representing a sequential decline of 24.9% but a YoY improvement of 6.8%, significantly missing consensus expectations by 15.0%. Pulp EBITDA decreased 25.8% QoQ but improved 9.0% YoY, while Paper EBITDA declined 18.6% QoQ and 6.7% YoY. The adjusted EBITDA margin contracted by 3.6 pp sequentially and 6.1 pp YoY to 42.1% in 1Q25, primarily pressured by an 8.2% increase in cash COGS per ton, reflecting higher wood and input costs, as well as the negative impact of concentrated maintenance downtimes on fixed costs.

From a credit perspective, the results were marked by a 1.3% increase in LTM adjusted EBITDA, a 9.7% reduction in total debt, and a 5.8% decrease in net debt. However, cash interest coverage was negatively affected by a 5.1% increase in LTM interest payments. As a result, gross leverage improved 0.5x sequentially to 4.1x, net leverage decreased 0.3x to 3.4x, but interest coverage worsened by 0.2x to 4.4x. Suzano’s liquidity remained strong, with R$24.15 billion in total liquidity, covering short-term debt by 5.6x and sufficient to meet its debt obligations through most of 2028. We note that management reiterated its priority of deleveraging, balancing shareholder returns with financial prudence. In 1Q25, Suzano limited share buybacks, focusing instead on not increasing net leverage.

Despite lower adjusted EBITDA, free cash flow before dividends and buybacks was positive at R$595 million, supported by lower capex of R$3.08 billion compared to R$3.86 billion in 4Q24 and consistently over R$4 billion between 2Q23 and 3Q24, along with a working capital release of R$1.31 billion. However, Suzano distributed R$2.19 billion in dividends and executed R$39 million in buybacks, resulting in a net free cash outflow of R$1.64 billion.

In Pulp, we expect the Chinese market to stabilize as spot prices in Asia have fallen to unsustainable levels below the marginal cost of production. This should support a recovery in order volumes and allow Suzano to benefit from normalized inventories and higher capacity, while continuing to support its customer base. We also expect a focus on reducing cash production costs in the coming quarters, with a target to return to 4Q24 levels. In Paper, prices are expected to remain stable throughout 2025, although pricing for paperboard and uncoated papers internationally may be affected by global market dynamics. We expect the company to prioritize lowering paper production costs, anticipating efficiency gains and reduced expenses in 2Q25 as maintenance downtimes subside and recent operational upgrades take effect.

As a result, we expect the combination of healthier pulp prices, higher sales volumes from the Ribas unit, normalized capital expenditures, lower costs, and a clear commitment to deleveraging to strengthen Suzano’s credit profile in 2025. This trend is likely to persist in the coming years, as no significant additional supply is projected to come online.