Suzano 1Q26: Pulp Pricing Recovery Tempered by FX and Volume Drag

Neutral maintained as strong liquidity and cost leadership support credit quality, while tighter spreads and elevated leverage limit upside.

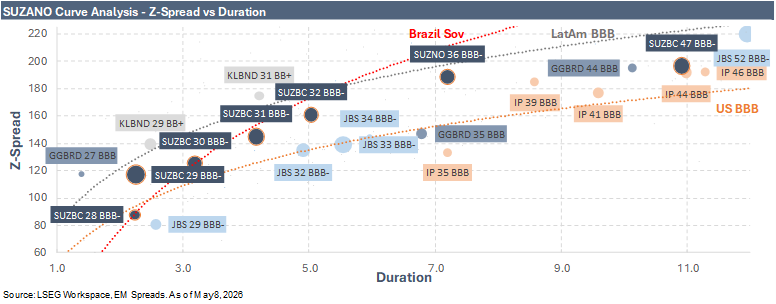

We maintain our Neutral recommendation on Suzano. We continue to view Suzano as a high-quality BBB- LatAm credit, supported by global cost leadership in hardwood pulp, strong liquidity, a diversified revenue base, and disciplined financial policy. Valuation, however, remains the main constraint after the recent tightening. 1Q26 results were weaker on a headline basis, but the decline was driven mostly by normal first-quarter seasonality, lower shipments, BRL appreciation, and scheduled maintenance downtime rather than any deterioration in Suzano’s competitive position. Pulp pricing improved sequentially, cash costs remained structurally competitive, and liquidity remains strong, but leverage is still elevated and the credit remains exposed to pulp-cycle volatility and FX translation pressure.

The quarter reinforced the balance of the credit story. Suzano continues to benefit from scale, cost competitiveness, strong liquidity access, and a more supportive pulp pricing backdrop, while lower 2026 capex should help free cash flow recover as seasonal headwinds normalize. Potential non-core asset sales could provide an additional deleveraging lever, although we continue to view operating cash flow as the central driver of balance sheet improvement. At the same time, 1Q26 showed that higher USD pulp prices can still be diluted in reported BRL EBITDA by a stronger BRL, seasonal volume weakness, and scheduled maintenance effects. Gross leverage improved to 4.5x from 4.7x in December 2025, while net leverage remained broadly stable at 3.5x. That leaves the balance sheet supportive of the credit, but not yet strong enough to justify an Overweight recommendation. We therefore see free cash flow generation and gradual deleveraging as the key variables for any more durable re-rating.