Telecom 1Q25: Margin Gains Support Credit, But Telefónica Deal Still Central

Ongoing Regulatory and Integration Risks Persist, Though Improving Macro and Election Results Ease Political Risk, while Positive Quarterly Results Support the Credit

Key Insights and Recommendations

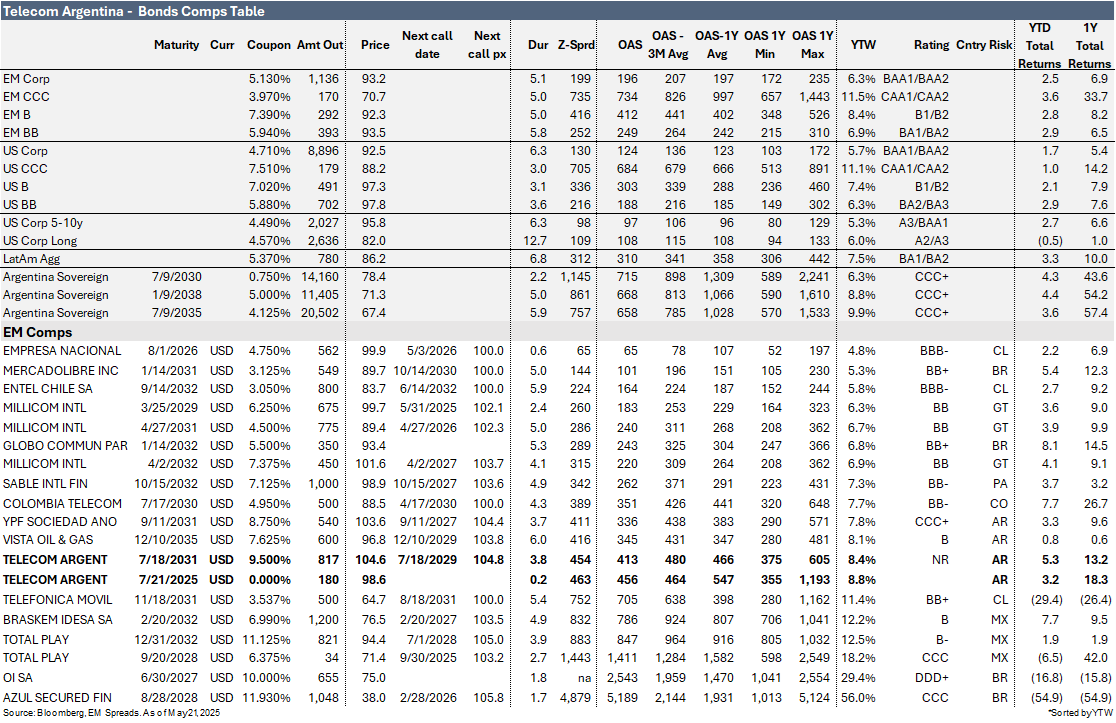

We maintain our Market Perform recommendation on Telecom Argentina (Caa1/B-/B).

Telecom Argentina reported a positive 1Q25, with healthy organic results and strong consolidated figures including Telefónica’s March numbers. Consolidated revenue increased 18.9% QoQ and 27.8% YoY to P$1,363 billion, exceeding market consensus expectations by 11.3%. The improvement was primarily driven by the integration of Telefónica Argentina, effective March 1, 2025. Service revenue rose 20.0% QoQ and 26.5% YoY to P$1,285 billion. Telecom’s service revenues excluding Telefónica increased 4.9% YoY, while Telefónica’s service revenues improved 17.1% YoY, primarily driven by real ARPU improvements across segments. Reported EBITDA rose significantly, up 50.5% QoQ and 39.9% YoY to P$452 billion. The EBITDA margin expanded 7.0 pp sequentially and 2.9 pp YoY to 33.1%, supported by operating costs increasing meaningfully below revenue growth, enhancing profitability.

From a credit perspective, the results reflected a 38.0% increase in gross debt and a 37.6% increase in net debt in USD terms sequentially. However, this was fully offset by a 56.6% sequential increase in LTM proforma EBITDA, which the company estimated at US$1.77 billion. As a result, gross leverage decreased to 2.3x as of March 2025 from 2.7x in December 2024, and net leverage improved to 2.1x from 2.4x over the same period. The company’s liquidity remains weak, with P$1,348 billion (US$1.26 billion) in short-term debt, representing 2.6x its cash position and 30.3% of total debt. Telecom’s cash and equivalents totaled P$519 billion (US$483 million). We note that the company lacks committed revolving credit facilities. Consequently, liquidity is not sufficient to cover short-term debt.

We view Telecom Argentina’s acquisition of Telefónica as a potentially transformative transaction for the local telecom landscape, with clear synergies in mobile and broadband services. While the acquisition may make strategic sense in the long run, it introduces immediate financial, regulatory, and operational risks. The government’s decision to suspend the deal underscores elevated regulatory risk, particularly around market concentration concerns. While the financing structure appears manageable in the near term, based on covenant compliance and proforma leverage trends, uncertainty around integration timelines and potential asset divestments to meet antitrust requirements could delay any meaningful credit upside.