Telecom Argentina 1Q26: Credit Improves, Upside Narrows

Stronger EBITDA, lower leverage, and refinancing support the credit, but valuation, liquidity, and TMA regulatory risk cap the trade

We move our recommendation on Telecom Argentina (B2/B-/B-) from Overweight to Neutral, while retaining the TECOAR 8.500% 2036 notes as our preferred expression within the curve for investors seeking to maintain exposure. The change is driven by valuation rather than a reversal in our fundamental view of the credit. Telecom remains an improving B rated Argentine credit, supported by TMA margin convergence, lower leverage, positive free cash flow, and a stronger maturity profile after the January refinancing. However, the front of the curve has rallied to levels that leave limited room for additional spread compression, given weak liquidity, unresolved regulatory risk around the TMA acquisition, and the dividend authorization in place through the end of 2026.

The 1Q26 results support the credit, but they do not justify keeping a broad issuer level Overweight after the move tighter. The key improvement was the quality of profitability across the enlarged platform, especially at TMA, where margin convergence progressed faster than we previously expected. That matters because the investment case after the acquisition depends less on near term revenue synergies, which remain constrained by the regulatory process, and more on cost discipline, efficiency gains, and the ability to narrow the profitability gap between the two platforms. The quarter also reinforced that the January refinancing was not just a technical event. Telecom’s maturity profile is now more manageable, and near-term refinancing pressure has declined.

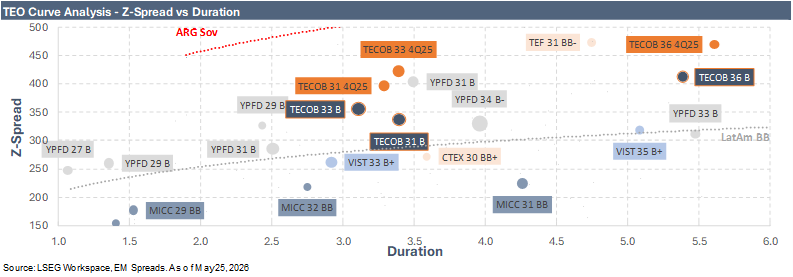

These positives would normally support a more constructive credit call, but in our view, they are already largely reflected in the front of the curve. The TECOAR 9.500% 2031 notes trade at $107.3, with 3.4 years of duration, 343 bps Z-spread, and 7.3% YTW. At 343 bps, the 2031s screen near one-year tights and well inside the 3M and 1Y averages of 406 bps and 483 bps, respectively. The TECOAR 9.250% 2033 notes trade at $106.2, with 3.1 years of duration, 362 bps Z-spread, and 7.4% YTW. The current Z-spread is also near the tight end of its one-year range and well inside the 3M and 1Y averages of 422 bps and 504 bps, respectively. On a yield basis, the 2031s and 2033s yield meaningfully below the EM B Index YTW of 8.7%.

Keep reading with a 7-day free trial

Subscribe to EM Spreads to keep reading this post and get 7 days of free access to the full post archives.