Vista 1Q26: Production Scale and FCF Outlook Support Deleveraging Path

Raised guidance, higher pro forma EBITDA, and stronger FCF visibility underpin Overweight, with curve preference shifting

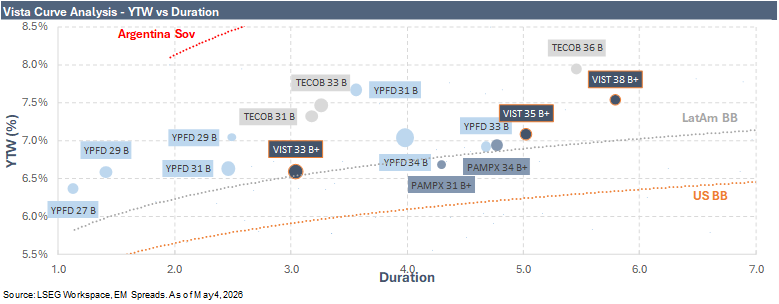

We maintain our Overweight recommendation on Vista Energy, but update our curve preference following the rally in the VISTAA 8.500% 2033 notes and the issuance of the new VISTAA 7.875% 2038 notes. After the recent spread compression, this is no longer a broad tightening call. The trade is now more about carry, curve selection, and choosing the right point of exposure. The 2033s remain a high-quality defensive hold for investors prioritizing lower duration and lower volatility. For new money, we prefer the VISTAA 7.625% 2035 notes as the more balanced expression. The newly issued 2038s also look attractive for accounts willing to add modest duration in exchange for the highest carry on the Vista curve.

Vista’s 1Q26 results continue to support the fundamental credit thesis. The quarter was marked by strong YoY production growth, resilient EBITDA generation, and a constructive guidance update. Management raised 2026 production guidance to 143 kboe/d from 140 kboe/d and left Capex unchanged at $1.5 billion to $1.6 billion. Under the $85/bbl Brent base case, Vista now expects $2.6 billion of adjusted EBITDA and $0.7 billion of free cash flow before the Equinor Transaction. Pro forma adjusted EBITDA is expected to increase to $3.0 billion after closing. This should support deleveraging, particularly as management has been clear that the next phase is about converting the enlarged production base into free cash flow and reducing net leverage toward approximately 1.0x by year-end 2026.

The key offset in 1Q26 was liquidity. Liquidity moved backward from the stronger year-end 2025 position, as cash and short-term investments no longer covered short-term debt at the end of March. The deterioration reflected an investment-heavy quarter, including VEISA-related working capital needs and acquisition funding. The subsequent $500 million 2038 senior notes issuance materially improved that snapshot and confirmed Vista’s continued access to international capital markets. Still, the lack of committed USD revolving credit facilities remains a constraint, and Al Mehwar’s reduced ownership limits the likelihood of external shareholder support in a stress scenario. Even with that caveat, Vista’s operating momentum, larger production base, and improved free cash flow outlook keep the Overweight case intact.