Vista 4Q25: Operational Momentum Reinforces Curve Preference

Shale scale, export-linked pricing and disciplined leverage support medium-term cash visibility

We maintain our Overweight recommendation on Vista Energy, with a continued preference for the VISTAA 8.500% 2033 notes as the most attractive way to express a constructive view on the credit.

4Q25 results reinforce Vista’s strong operating momentum, with continued production growth, solid EBITDA generation, and leverage remaining around 1.6x on a pro forma basis. We think the company maintains a robust business profile anchored in Vaca Muerta, supported by an oil-weighted portfolio, growing export exposure, and structurally improving unit costs following the ramp-up of midstream infrastructure. While the reduction of Al Mehwar’s stake to 2.77% removes a previously cited liquidity mitigant in a stress scenario, we believe Vista’s standalone fundamentals, a consistent track record of capital markets access, and improved short-term debt coverage support a resilient credit profile under our base case assumptions.

The acquisition of Equinor’s stakes in Bandurria Sur and Bajo del Toro further reinforces our constructive stance, as discussed in our recent note, “Vista Acquires Equinor’s Vaca Muerta Assets, Reinforcing Core Acreage Position.” The transaction increases pro forma production to roughly 150 kboe/d, enhances oil weighting and export exposure, and adds low-cost barrels at attractive implied valuation metrics. We view the leverage impact as broadly neutral despite higher absolute debt, with pro forma gross leverage remaining around 1.9x and net leverage increasing only modestly to approximately 1.7x, while scale and hard currency EBITDA increase meaningfully. In our view, the transaction improves medium-term cash flow durability and enhances visibility on the development plan, further strengthening the fundamental case for holding duration in the belly of the curve.

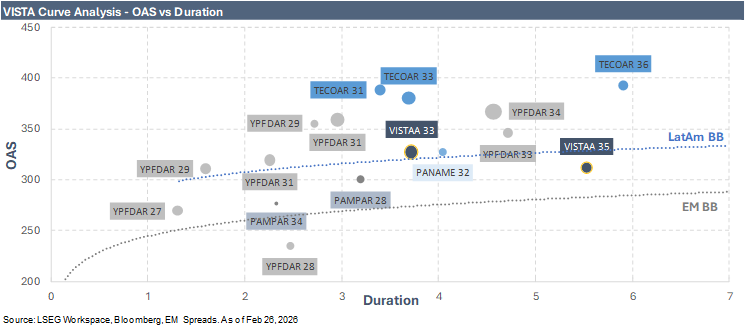

From a curve positioning standpoint, the VISTAA 8.500% 2033 notes trade at an OAS of 327 bps, with a 3.7-year duration and a yield to worst of 7.0%, while the VISTAA 7.625% 2035 notes trade at 312 bps OAS, with a 5.5-year duration and a yield to worst of 7.2%. In our view, the modest yield pickup on the 2035s does not adequately compensate for nearly two additional years of duration and higher exposure to Argentina risk. The 2033s offer a more balanced combination of carry and lower volatility, in what we view as the most efficient part of the curve for investors seeking exposure to Argentina’s shale growth story without assuming incremental duration risk.