YPF 4Q25: Downstream Strength and Shale Scale Offset Price Headwinds

Structural mix upgrade enhances operating leverage and margin durability, while liquidity constraints and Argentina risk guide disciplined bond selection

We maintain our Overweight recommendation on YPF (B2/B-/CCC+), as 4Q25 confirms that the structural transformation of the asset base is translating into a more resilient credit profile, even if liquidity remains the key constraint.

We think 4Q25 reinforces the structural improvement in the operating profile. The transition toward a lower cost, more oil weighted portfolio continued to gain traction, with shale oil production up 41.9% YoY, representing 71.5% of total crude, and total lifting costs down 44.2% YoY. This mix shift, together with the sharp recovery in downstream profitability, helped lift adjusted EBITDA 53.0% YoY. The accelerated exit from mature conventional fields, combined with Vaca Muerta scale and midstream and export projects, including VMOS, with first oil expected in December 2026 at ~180 kbbl/d and ramping to ~550 kbbl/d by 3Q27, and Argentina LNG, with FID targeted for 2026, continues to de risk the asset base and improve through cycle margin resilience. This supports a more durable hard currency cash generation profile as export capacity expands and strengthens the standalone credit profile.

That said, we continue to view liquidity and refinancing execution as a constraint. Liquidity remains weak, with short term debt of $2.36 billion equivalent to 197% of cash plus short term investments, and roughly $2.1 billion of maturities scheduled for 2026. We think YPF’s continued market access helps offset this constraint, including the $500 million 2031 re tap in 4Q25, the $700 million export backed syndicated loan with $650 million undrawn as of February 2026, and the $550 million 2034 re tap in January 2026 that was partly used to prepay the $324 million CAF A/B loan. Divestment execution also remains an important part of the liquidity bridge, including proceeds collected from the Profertil stake sale and the signed sale of Manantiales Behr, which remains subject to closing.

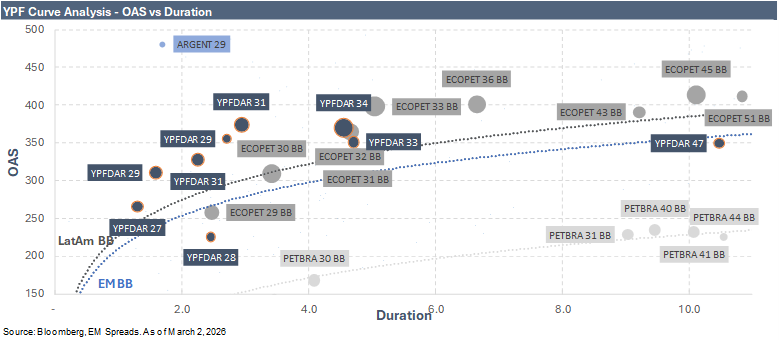

The balance of the story remains Argentina risk. Despite improving operating fundamentals, sovereign and policy dynamics continue to act as the dominant overlay and can reprice the curve quickly. As the 2027 presidential cycle approaches, we expect political volatility to reemerge, limiting the scope for sustained decoupling in longer dated bonds and reinforcing the need for disciplined bond selection and careful duration control.