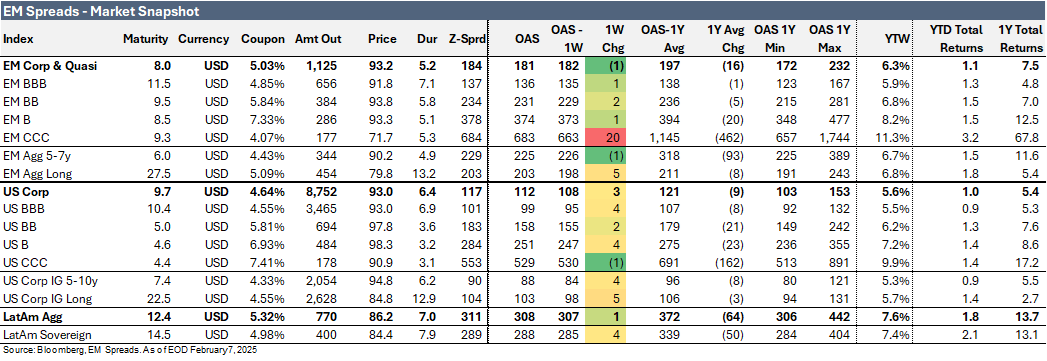

Market Snapshot

The LatAm Aggregate Index expanded modestly by 1 basis point (bp) to 308 bps in the week ending Friday, February 7, 2025. Meanwhile, the broader Emerging Market Index tightened by 1 bp to 181 bps, while the broader U.S. Index widened by 3 bps to 112 bps. Notably, the EM CCC Index widened significantly by 20 bps to 683 bps, following a meaningful tightening of approximately 80 bps the previous week. Equity markets in the region showed mixed performance. Argentina's Merval Index dropped 5.8%, Brazil's Ibovespa Index declined 1.2%, and Mexico's Mexbol Index rose 3.1%. In the U.S., the S&P 500 Index edged down 0.2% for the week.

In commodities, WTI crude oil traded at $74.70 per barrel (-2.7% weekly), while Brent crude settled at $71.00 per barrel (-2.1%).

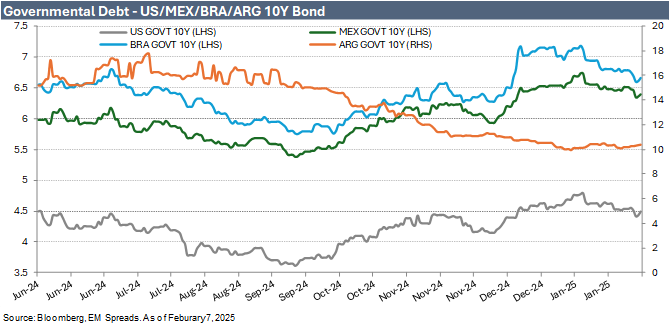

Turning to bond yields, U.S. Treasuries saw mixed movements. The 10-year yield declined 4 bps to 4.49%, while the 5-year yield rose 2 bps to 4.35%. In Latin America, the yield on the 10-year Mexican government bond dropped 12 bps to 6.40%, the 10-year Brazilian government bond fell 12 bps to 6.66%, and the 10-year Argentine government bond rose 20 bps to 10.41% over the week.

Weekly News

1. Cemex 4Q24: A Solid EM Credit, But Tariff Overhang Limits Near-Term Potential

On February 7, 2025, we published our Cemex 4Q24 results report.

We maintain our Market Perform recommendation on Cemex. We continue to view Cemex as an attractive emerging market credit story, supported by credit-positive strategic priorities, a commitment to strengthening its credit profile, and healthy cash generation capacity. However, current spread levels appear fair and do not offer an attractive entry point, particularly given the potential risk of U.S. tariffs on Mexican imports, which could significantly impact the broader Mexican economy. That said, spreads may be more appealing to investors who see tariff concerns as overstated or unlikely to materialize. We would keep the name on our watchlist for potential investment should this risk of U.S. tariffs subside.

Within Cemex’s capital structure, we prefer the CEMEX (BBB-/BBB-) 5.20% 2030 notes, which trade wider than the Mexican sovereign, the EM BBB index, and comparable peers. However, we do not anticipate these notes to outperform in the near term.

2. YPF Refines Focus with Asset Sales and Strategic Acquisition

Argentina’s state-run oil company YPF has completed two key transactions in line with its strategy to focus on the Vaca Muerta formation while divesting non-core assets.

On February 3, 2025, YPF sold YPF Brasil Comércio de Derivados de Petróleo to GMZ Holding and IGP Holding Participações for $2.3 million. The sale grants the buyers licensing rights to produce and sell lubricants under the YPF brand in Brazil.

Separately, on January 29, 2025, YPF finalized the $327 million acquisition of Mobil Argentina from ExxonMobil and QatarEnergy. Mobil Argentina holds a 54% stake in the Sierra Chata concession, a key natural gas asset in Vaca Muerta, with Pampa Energía controlling the remaining interest. The newly acquired entity has been renamed SC Gas, with YPF as its sole shareholder.

Credit Impact: These transactions align with our expectations, reinforcing YPF’s commitment to sharpening its focus on Vaca Muerta while shedding non-core assets. The company is executing its strategy, which is a positive development as it seeks to enhance operational efficiency and strengthen its position in Argentina’s energy sector.

3. YPF: S&P Upgrades Argentine Corporates Amid Improved Transfer and Convertibility Risk

On February 5, 2025, S&P Global Ratings upgraded YPF’s local and foreign currency ratings, along with those of eight other Argentine companies, to B- from CCC. Additionally, three companies were raised to CCC+ from CCC, while one entity’s rating was affirmed at CCC. All affected issuers received stable outlooks. The upgrades follow an upward revision of Argentina’s transfer and convertibility (T&C) assessment to B- from CCC, reflecting a modest reduction in the perceived risk of government interference in capital flows. However, S&P cautioned that Argentina’s economic conditions remain fragile, and external liquidity remains challenging despite some improvement.

While the sovereign’s refinancing path in the coming quarters remains uncertain, Argentine companies’ ability to service foreign-currency debt will depend on their access to and ability to transfer hard currency. The upgrades indicate some positive momentum, but fundamental risks persist.

Credit Impact: The rating actions align with our expectation that improving macroeconomic conditions in Argentina would support a stronger credit profile for YPF. We believe that Argentina’s improving macroeconomic conditions, particularly in terms of GDP growth and inflation, will enhance the country’s credit profile and increase the likelihood of removing capital controls, which should support YPF’s operations. Additionally, the improved conditions are expected to improve the company’s access to hard currency, easing refinancing risks and enhancing its ability to manage dollar-denominated obligations.

See Also:

Cemex (February 7, 2025): Cemex 4Q24: A Solid EM Credit, But Tariff Overhang Limits Near-Term Potential.

Cemex & Pemex (February 5, 2025): U.S. Tariffs and Their Potential Impact on Cemex and Pemex.

Pemex (January 31, 2025): Lack of Concrete Action Weights on the Outperform Thesis.

Suzano (January 30, 2025) Initiation coverage report.

YPF (January 8, 2025): Recommendation on YPF's new USD 9NC4 unsecured notes.

Vista Energy (December 18, 2024): New issue snapshot.

YPF (December 3, 2024): Initiation coverage report.

Disclaimer

Opinions presented in this report are based on and derived primarily from public information that EM Spreads LLC ("EM Spreads," "We," or "Our") considers reliable. Still, we make no representations or warranty regarding their accuracy or completeness. EM Spreads accepts no liability arising from this report. No warranty, express or implied, as to the accuracy, timeliness, completeness, or fitness for any particular purpose of any such analysis or other opinion or information is given or made by EM Spreads in any form.

All information contained in this document is protected by Copyright law, and none of such information may be copied, repackaged, transferred, redistributed, resold, or stored for subsequent use for any such purpose, in whole or in part, by any person without EM Spreads’ prior written consent. All rights reserved. Reproduction of this report, even for internal distribution, is strictly prohibited. The content shall not be used for any unlawful or unauthorized purposes.

This content is provided on an "as is" basis and should not be regarded as a substitute for obtaining independent advice. EM Spreads disclaims all express or implied warranties, including, but not limited to, any warranties of merchantability or fitness for a particular purpose or use, freedom from bugs, software errors, or defects, that the content’s functioning will be uninterrupted or that the content will operate with any software or hardware configuration. Investors must determine the appropriateness of an investment in any instruments referred to herein based on the merits and risks involved, their own investment strategy, and their legal, fiscal, and financial position. As this document is for information purposes only and does not constitute or qualify as an investment recommendation or advice or as a direct investment recommendation or advice, neither this document nor any part of it shall form the basis of or be relied on in connection with or act as an inducement to enter, any contract or commitment whatsoever. Nothing in this report constitutes investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise a personal recommendation to you.

The opinion contained in this report may not be suitable for your specific situation. Investors are urged to contact their investment advisors for individual explanations and advice. EM Spreads does not offer advice on the tax consequences of investments, and investors are urged to contact an independent tax adviser for individual explanations and advice. In no event shall EM Spreads be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special, or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of this report.

This document may contain forward-looking statements that involve risks and uncertainties. Actual results may differ materially from those expressed or implied in such statements. EM Spreads undertakes no obligation to update any forward-looking statements to reflect events or circumstances after the date of this document or to discontinue it altogether without notice. EM Spreads reserves the right to modify the views expressed herein without notice.

The content in this report is provided to you for information purposes only. EM Spreads’ opinions and analysis are not recommendations to purchase, hold, or sell any securities or to make any investment decisions and do not address the suitability of any security. EM Spreads assumes no obligation to update the content following publication in any form or format. The content in the report shall not be relied on and is not a substitute for the skill, judgment, and experience of the user, its management, employees, advisors, and /or clients when making investment and other business decisions. EM Spreads has not taken steps to ensure that the securities referred to in this report are suitable for any investor.

This report is not directed to or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any locality, state, country, or other jurisdiction where such distribution, publication, availability, or use would be contrary to law or regulation or which would subject EM Spreads to any registration or licensing requirement within such jurisdiction. No person should review or rely on this report if such review or reliance would require EM Spreads to obtain any registration or license in any such jurisdiction.

All estimates and opinions expressed in this report reflect the analysts' independent judgment as of the issue's date about the subject company or companies and its or their securities. No part of the analyst's compensation was, is, or will be directly or indirectly related to this report's specific recommendations or views. The research analysts contributing to the report may not be registered /qualified as research analysts with any regulatory or government body or market regulator.